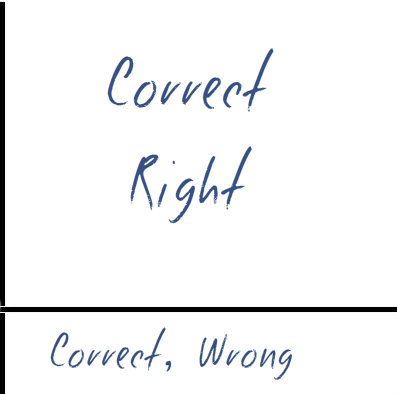

There is a difference between correct/incorrect and right/wrong decisions, and over the long run it’s much more important to be correct than right.

I discovered this framework in What I Learned Losing a Million Dollars by Jim Paul and Brendan Moynihan.

The correct/incorrect distinction is based on the Expected Value (EV) of the decision.

Right/wrong is based on whether a decision works out in a particular instance.

For example, say you’re playing poker and you have the option of paying $100 with a 20% chance of winning $1000.

The expected value is $200 ($1000 x 20%).

The correct decision is to make the bet—you pay $100 for an expected value of $200 – positive EV. If you knew you were going to face that bet 100 times and you made it every time, you would come pretty close to doubling your money (per the law of large numbers).1

If you win in that instance, then it’s right. If you lose, then it’s wrong.

I’ll use poker as an analogy because it’s a little more clear cut, but all of the principles apply to entrepreneurship and investing.

A few interesting points worth highlighting:

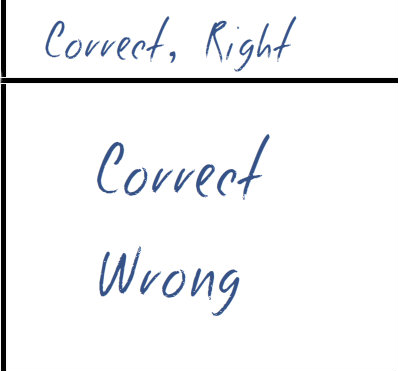

1. Quantitative vs Qualitative Value of Outcomes

The player in this poker game making the correct decision is going to be wrong the majority of the time. By quantity, 80% of his decisions are wrong. However, by outcome, he will double his money.

Assuming the player was correct every time, If we were to redraw the matrix and weight the quadrants according to quantitative vs qualitative, it would look like this:

Qualitative Value of Outcomes -Matrix redrawn so each square is sized as a percent of net winnings.

Quantitative Value of Outcomes – Matrix redrawn so each square is sized as percent of decisions:

The poker player may lose $100 on nine hands out of 10 (making his winning percentage 10%) but win $1800 on a single hand (making his net winning $900). Even though he loses nine times out of 10, he still doubles his money.

Warren Buffett’s investments firm, Berkshire Hathaway has assets totalling around $526 billion, but the vast majority of that came from a small number investments (Disney, the Washington Post, and Geico).

2. Successful people are wrong most of the time.

They’re just wrong on positive Expected Value decisions. Paying $100 with a 20% chance of winning $1000 means you lose 80% of hands you play, but you still double your money over time. This is often obscured because when you read someone’s two-paragraph bio, you only hear about the wins, even if that’s only .1% of all the outcomes they’ve gotten.

These are good decision making skills.

Why?

3. You are biologically wired to focus on being right rather than being correct.

If you’re wandering around the African savannah there aren’t any events with non-linear outcomes. If you kill a gazelle, you get one gazelle worth of meat. If you bet $100 in a poker game, you could win $1000. The size of the output does not correlate linearly with the input. It would be the equivalent to having one gazelle per herd which somehow produces ten gazelles worth of meat when you kill it.

Poker seems to be the best analogy to use because it’s widely perceived as “risky” or a “game of chance.” If you don’t understand the game and you only play a few hands, poker does largely seem to be a game of chance. There’s no room for the law of large numbers or skill to take effect. The people I know who are skilled at the game seem to be able to predict their incomes with remarkable accuracy.

However, the same principles are true in investing and entrepreneurship.

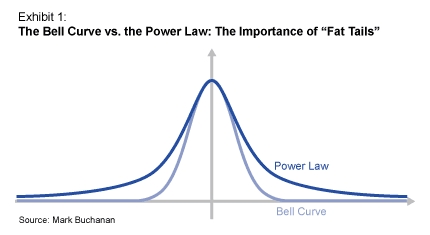

4. Fat Tails are in full effect.

The margin emerges at the far ends of the graph precisely because most people are more concerned with being right than being correct.

An excerpt from Michael Lewis’s Liar’s Poker illustrates the point. He’s explaining the trading strategy of a co-worker who made money simply by preying on other investor’s fear of being wrong even if it was correct.

First, when all investors were doing the same thing, he would actively seek to do the opposite. The word stockbrokers use for this approach is contrarian. Everyone wants to be one, but no one is, for the sad reason that most investors are scared of looking foolish. Investors do not fear losing money as much as they fear solitude, by which I mean taking risks that others avoid. When they are caught losing money alone, they have no excuse for their mistake, and most investors, like most people, need excuses. They are, strangely enough, happy to stand on the edge of a precipice as long as they are joined by a few thousand others. But when a market is widely regarded to be in a bad way, even if the problems are illusory, many investors get out. A good example of this was the crisis at the U.S. Farm Credit Corporation. It looked for a moment as if Farm Credit might go bankrupt.

Investors stampeded out of Farm Credit bonds because having been warned of the possibility of accident, they couldn’t be seen in the vicinity without endangering their reputations. In an age when failure isn’t allowed, when the U.S. government had rescued firms as remote from the national interest as Chrysler and the Continental Illinois Bank, there was no chance the government would allow the Farm Credit bank to default. The thought of not bailing out an eighty-billion-dollar institution that lent money to America’s distressed farmers was absurd. Institutional investors knew this. That is the point. The people selling Farm Credit bonds for less than they were worth weren’t necessarily stupid. They simply could not be seen holding them. [Emphasis mine]

Because institutional investors have to raise money and because most people don’t understand risk, they have to worry about being wrong instead of worrying about being correct.

A similar example I’ve heard from venture capitalists is that companies that are attractive investments must have both huge potential and seem like terrible ideas. Longer lasting batteries have huge potential right now, but everyone knows that so there isn’t a lot of margin left.

Facebook, on the other hand, sounds like a terrible idea. Let’s make a site for college kids (terrible market, they’re all broke, and how will that ever make money?). Likewise with AirBnB, a site to help strangers sleep in your house!

There’s a spectrum here as well that doesn’t just include billion dollar companies. Lots of highly profitable, bootstrapped companies are relatively larger-potential and worse-sounding ideas than others the founder was initially working on.

If no one thinks your idea is stupid, there’s probably not a lot of margin left in it.

If literally everyone thinks your idea is stupid, then it is. You need at least a few customers to get a business started.

Caveat: Don’t die.

Always cap your downside to make sure your exposure is non-fatal. Going all-in on a positive EV decision where the odds of winning are only 10% is risky. If hiring someone without them being a superstar is going to make you go into negative cash flow, then it’s not a good idea.

This seems to lead to a simple two question process for evaluating opportunities.

- Will this kill me? (literally or metaphorically)

- If not, what’s the correct (positive expected value) decision?2

Good decision making skills: specific examples:

Since discovering this framework, I’ve found it broadly applicable. Here’s a few specific examples to get you started.

Dating/Friends – If you go on 200 dates in a lifetime, typical results might be that 100 are terrible, 50 are bad, 30 are meh, 19 are good, and 1 is great.

So you’ve got a 0.5% chance of being right, but it’s still a correct decision to go on a bunch of dates, because the payoff from one right date is worth the 99.5% of times you’re wrong. Same with meeting people and the chance of them becoming long time friends or business partners.

Hiring – In my experience, about 2-7% of applicants are even worth reading the whole application, and 1-2% are worth getting on the phone for an interview. Then only a certain percentage of hires work out.

However, hiring and management is so high leverage that it’s still the correct thing to do.

Business Conferences – Most conferences are terrible, but the few good ones are so good, and the people you meet are so awesome that it’s the correct decision to go to a lot of conferences,

Even though most new conferences you go to will be terrible, it’s worth it to go to a bunch to figure out the best ones.

Careers – In the last five years, I’ve dabbled (to some extent) in law, academia, medical interpreting, teaching English, SEO, project management, SEO again, email marketing, copywriting, B2B software sales, healthcare consulting, marketing consulting, business systems consulting, and writing books.

Even if I’m being generous with myself, my batting average is poor. However, my “slugging percentage” is pretty decent. Most of them haven’t succeeded, but the ones that have worked out well enough to make up for all the failures.

Are you focused on being correct or being right? There’s more margin (over the long run) in correct.

Footnotes

- Both Tynan and Billy Murphy have great articles expounding on Expected Value.

- I might also add “does this play to my strengths” or “is this near my circle of competence” to that list when relevant.