Buy The Innovator’s Dilemma on Amazon.

The Innovator’s Dilemma is a book about how innovation happens (or, more often, doesn’t happen).

There are many such books and most of them are bad. This one is interesting because of Christensen’s detailed research on various technologies (primarily computing) and because of a counter-narrative conclusion: successful companies are disrupted not because they get complacent or lazy. They get disrupted because they are actually very, very good at what they do.

It’s important to know Disruption, in the sense Christensen uses it, is when a simpler, cheaper, lower margin product starts to take off for a fringe use case.

This is a bit confusing as it is not how we use the term in everyday speech. For instance, Uber and Tesla would not be considered disruptive innovations under Christensen’s framework because they started with premium, higher-priced products. The base price of Tesla’s first model, the Roadster, was $80,000-120,00, squarely at the high-end luxury part of the market. Similarly, Apple was not disruptive because they have a premium product line.

However, the I think you can generalize Christensen a bit to say that innovation happens by coming at a market in a new direction which does not make sense in the context of existing market structure. Price is one way to do this, but there are others.

There is a general cycle Christensen identifies:

- A disruptive technology is developed

- Customers for it were found

- An organization was grown around satisfying the needs of those customers

- These companies tend to gradually move up market where higher profit margins were.

- This creates opportunity for a more entry level product

Take the spreadsheet as an example. Microsoft’s Excel is one of the most successful products of all time. It was developed by Microsoft and sold to their customers. As a result, Excel has gotten more and more powerful and robust, offering more functionality that Microsoft’s business customers needed and they were willing to pay up for it.

However, these changes also made it harder to learn and less approachable for the novice. Google Sheets came in as a more lightweight version that harnessed a new technology, the internet, to make it more collaborative. As a result, most people today start using Google Sheets instead of Excel because it’s more approachable for basic use cases.

With the overview of his thesis laid out, I’ll present a few key themes on innovative thinking from the book and expand on how I think they can be successfully applied.

Innovative Thinking Requites thikning in terms of Paradigm Shifts

What we see in a new technology depends both upon what we are looking at and what our previous experience has taught us to see. Without such experience, there can only be, in nineteenth-century philosopher and psychologist William James’s phrase, “a bloomin’ buzzin’ confusion”.

European astronomers first started noticing changes happening in the cosmos in the second half of the 16th century. By contrast, Chinese astronomers had recorded the appearance of sunspots, news stars, and comets centuries before. Why? Western astronomers had pretty much the same technology for mapping the stars as the Chinese had centuries before. What they lacked was an accurate view of the universe to go along with that technology.

In 1543, Nicolaus Copernicus published a book that offered a new view of how the Cosmos worked, proposing that the Earth orbited the Sun. The Western astronomers that adopted Copernicus’s idea continued looking at the sky with the same instruments as everyone else, but they saw the cosmos in a new way.

For astronomers familiar with Copernicus, the subsequent years were marked by frequent and significant discoveries. Meanwhile, those that did not adopt the model continued to stagnate. It was as if the two groups were living in different universes.

Maybe you’ve had the experience of going for a swim in the ocean, only to be surprised by the force of the waves. The water looks almost gentle on the surface, but the appearance belies the power and strength of what’s happening underneath. Technological revolutions are no different.

They tend to feel disorienting, confusing, overwhelming, or sometimes just dumb at first. But once you start to swim with them rather than against them, new possibilities are unlocked—your universe begins to change. To do this requires updating your model for how the Universe works. This is not just true of astronomy, but any new technology.

The first computers were constructed in the 1920s, made of physical rods and poles that represented states in a calculation. Each rod and pole had to be moved around and configured for whatever calculation was being performed. A simple calculation set up could take days to assemble.

At the time, computing was looked down on by mathematicians and scientists at institutions like MIT because it was seen as “just arithmetic.” To do a simple algebra problem, they had to physically arrange a garage-sized room of poles and rods. Doesn’t seem like a terribly useful technology, does it?

With the benefit of hindsight, this seems to be obviously wrong and surely you wouldn’t make such a mistake?

But this is all too common and most people fall into the same. Chris Dixon’s post titled What the smartest people do on the weekend is what everyone else will do during the week in ten years is self-explanatory. He explains

Many breakthrough technologies were hatched by hobbyists in garages and dorm rooms. Prominent examples include the PC, the web, blogs, and most open-source software.

You can probably add cryptocurrency, psychedelics and probably 3d printing to that list as well if you wanted to update it.

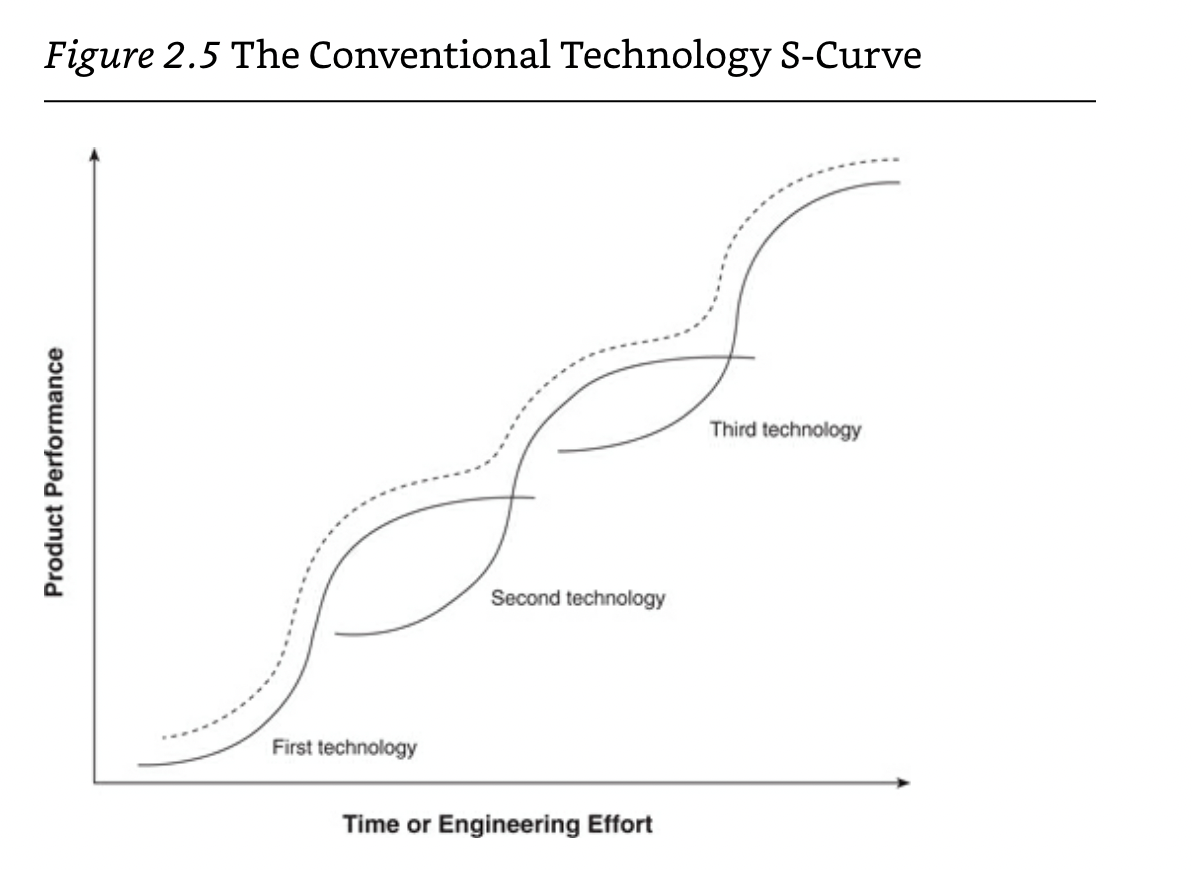

We tend to think of technology developing as a series of S-Curves. One technology peaks and another finds some way to improve on it and ramps up again.

However, this can be a bad framework because the vertical axis for a disruptive innovation, by definition, must measure different attributes of performance than those relevant in established value networks.

For example, the most common measure for desktop computers was computational power – RAM, Processors Speed and so on. Mobile phones were not more computationally powerful than laptops or desktops, they were far inferior on that axis and so led to many disregarding them.

They competed along a different axis: portability. The killer feature was it was a computer you could put in your pocket. You didn’t need a lot of computing power to play music or look at Facebook or order a rideshare, you just needed it to be small enough to carry with you all the time.

When you are looking at a new technology, do not think of it in terms of “what existing use case can this serve better,” rather, the question is “what new, emergent use case does this facilitate”.

Once you had a computer with a GPS in your pocket, ride-sharing apps suddenly made sense. That was a new dimension unlocked by smartphones, not an improvement on an existing one.1

Comparing cryptocurrency’s potential to the traditional financial infrastructure, say thinking of it as a money transmitter like Western Union is not very helpful. To the extent it is successful, it will be because it competes along a new axis, not merely marginal improvements on an old one (though the two are not mutually exclusive).

Get out of the Building: Market Driven Innovation

Economically disruptive innovation is always innovative relative to the needs of the market, not the technologist or the existing customer.

As Christensen notes:

Generally disruptive innovations were technologically straightforward, consisting of off-the-shelf components put together in a product architecture that was often simpler than prior approaches.”

I sometimes refer to these as “duh businesses” – when you hear about them you think how dumb it seems no one thought of them earlier as they fill an obvious place in the market.

These businesses tend to be identified not by careful market research, but by careful observation of how the needs of consumers are changing.

“Markets for disruptive technologies often emerge from unanticipated successes, on which many planning systems do not focus the attention of senior management. Such discoveries often come by watching how people use products, rather than by listening to what they say. I have come to call this approach to discover the emerging markets for disruptive technologies agnostic marketing, by which I mean marketing under an explicit assumption that no one—not us, not our customers—can know whether, how, or in what quantities a disruptive product can or will be used before they have experience using it.”

A common tendency is to view innovation as something that requires technological advancement. Sometimes that’s true but oftentimes it’s more about repurposing existing technology in a way that jives with the market more.

“In the instances studied in this book, established firms confronted with disruptive technology typically viewed their primary development challenge as a technological one: to improve the disruptive technology enough that it suits known markets. In contrast, the firms that were most successful in commercializing a disruptive technology were those framing their primary development challenge as a marketing one: to build or find a market where product competition occurred along dimensions that favored the disruptive attributes of the product.”

The book Blue Ocean Strategy is a pretty good example of this type of thinking. It provides a framework for looking at markets and working back to what characteristics people are looking for in their products.

It offers a number of case studies including Yellowtail wine which made no material technological progress but positioned itself differently than other wine brands had.

Steve Blank, the founder of the customer development movement, called this product development strategy “Getting out of the building.” What most people need to do is not think harder about where innovation lies, they need to go talk to a bunch of people about how they are using the product or similar products and understand their needs.

An important point here is that you don’t just want to talk to existing customers. Microsoft talked to their customers about Excel and what they told them was that they wanted a more powerful excel. You have to also talk to other potential customers that may not seem particularly valuable today.

“The established firms steadfastly focused their innovative investments on their customers. Subsequent chapters will show that this strategic choice is present in most instances of disruptive innovation. Consistently, established firms attempt to push the technology into their established markets, while the successful entrants find a new market that values the technology.”

Be Mindful of your Organization Structure

Maybe the most overlooked piece of how innovation actually happens is the importance of organizational structure.

“My findings consistently showed that established firms confronted with disruptive technology change did not have trouble developing the requisite technology: Prototypes of the new drives had often been developed before management was asked to make a decision. Rather, disruptive projects stalled when it came to allocating scarce resources among competing product and technology development proposals.”

Stage 3 in Christensen’s innovation framework is that once a big innovation has been developed, an organization is built around continuing to develop and profit from that innovation.

However, this creates a particular internal dynamic that is hard to change. Once you have a sales team then it is hard to launch a product that doesn’t require sales.

This was a big trend with marketing tech in the 2010’s – you had all these big legacy companies (Hubspot, Marketo, would maybe through Salesforce in there, etc.) which were built on the back of their enterprise sales teams going out and selling big contracts.

Once APIs started to become more widely used, it was a lot easier to just buy the small, use-case-specific solutions that a given marketing team needed and link them together via APIs. You didn’t need your SEO tracker, content management system, email marketing service and landing page builder to be bundled into one service. You could just sign up for what you needed and then integrate them.

This is the core of Christensen’s counter-narrative conclusion: the problem was not that companies which got disrupted were bad at their jobs, they were actually very good at them.

“The reason is that good management itself was the root cause. Managers played the game the way it was supposed to be played. The very decision-making and resource-allocation processes that are key to the success of established companies are the very processes that reject disruptive technologies: listening carefully to customers; tracking competitors’ actions carefully; and investing resources to design and build higher-performance, higher-quality products that will yield greater profit.”

Organizations can be thought of as a pattern of interactions. They create value as they transform inputs (people, equipment, technology, brand equity, energy, capital) into products and services of greater worth.

These patterns of interactions tend to be formalized at three layers:

- Software – code executing business processes.

- Written Processes – documented SOPs and the like of how things get done. Processes include things like product development, procurement, market research, budgeting, planning, and hiring.

- Guiding Principles and Culture – less formalized but reliable cultural attributes and principles for how people make decisions.

One of the dilemmas of innovation is that guiding principles and processes are really valuable. They ensure that employees perform recurring tasks in a consistent way, time after time and so the value delivered to the consumer is consistent and predictable which enhances the brand perception.

This means that the very mechanisms through which most organizations create value are intrinsically inimical to change. The processes that make an organization good at outsourcing design cannot also make it good at doing design in-house.

Guiding principles are an extension of this. An organization’s values are the standards by which employees make prioritization decisions—by which they judge whether an order is attractive or unattractive; whether a customer is more important or less important; whether an idea for a new product is attractive or marginal; and so on.

The only viable solution seems to be that you want to separate the people working on the innovation from the rest of the organization. Having a team of people working part time on the disruptive technology and part time on chugging things along never seems to work. They get dragged back into the culture of the bigger organization.

Most of the successful examples of disruption then happen within an entirely different organizational structure. In some cases, this is a new startup or business (sometimes started by someone that left the existing business) or sometimes it is done within the same company but at a separate office with separate people.

It is probably best that they be in an entirely different office to isolate them from the culture with a staff that is totally responsible for that.

You tend to “Ship Your Org Chart” – meaning your products tend to match the organization of the company that built them. Companies with big sales teams tend to develop complex products that require big sales teams because the sales team has a vested interest in seeing that’s the case.

Most large and sophisticated companies still mess this up. A good way for an acquiring company to tank the value of an acquisition is to merge the acquisition into their existing culture and processes, yet this is what most do.

For this to work within an existing organization usually requires a large amount of top down approval from the CEO and leadership team.

In our studies of this challenge, we have never seen a company succeed in addressing a change that disrupts its mainstream values absent the personal, attentive oversight of the CEO—precisely because of the power of processes and values and particularly the logic of the normal resource allocation process. Only the CEO can ensure that the new organization gets the required resources and is free to create processes and values that are appropriate to the new challenge.

Amazon is probably the best company in the world at this as their organizational structure of smaller, two-pizza teams seems to naturally lend itself to internal disruption. For example, when Amazon started working on the Kindle, they didn’t do it within the book department, they did it with an entirely different team at an entirely different physical location that wasn’t interacting at all with the main book department.

When managers aligned a disruptive innovation with the “right” customers, customer demand increased the probability that the innovation would get the resources it needed. They placed projects to develop disruptive technologies in organizations small enough to get excited about small opportunities and small wins. They planned to fail early and inexpensively in the search for the market for a disruptive technology. They found that their markets generally coalesced through an iterative process of trial, learning, and trial again. They utilized some of the resources of the mainstream organization to address the disruption, but they were careful not to leverage its processes and values.

Appreciate the power of Compounding and the Star Principle

Many large companies adopt a strategy of waiting until new markets are “large enough to be interesting.”

A better strategy is to look at markets growing fast such that they will become interesting soon. Chris Dixon’s aforementioned heuristic about what smart people are doing on weekends is one good example.

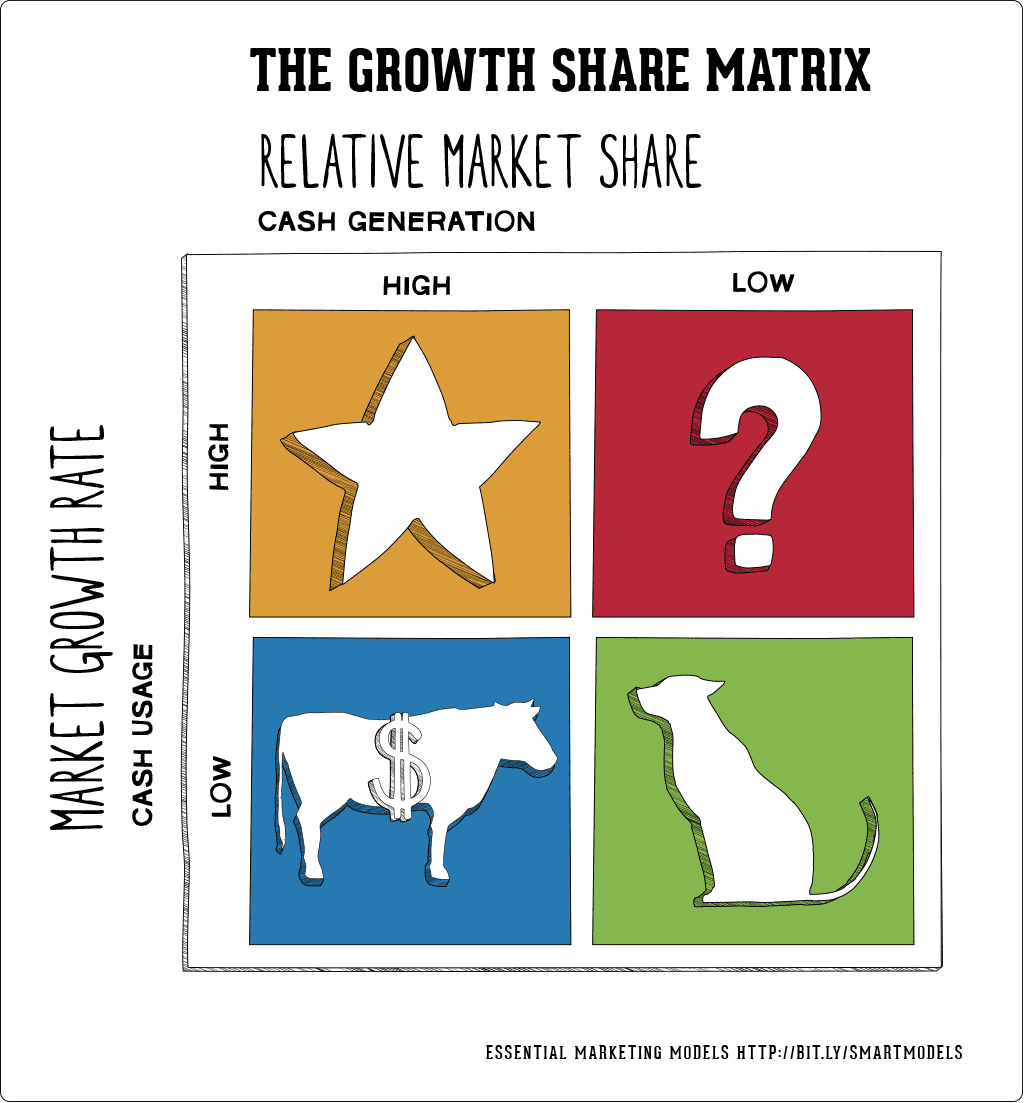

Another helpful way I’ve found for thinking about this is the Star Principle, part of a framework developed by Boston Consulting Group and expounded on by Richard Koch.

Basically, it says all businesses (or divisions of a larger business) can be categorized in a 2×2 of growth rate and market share along each axi.

Businesses in low growth rate industries with little market share are dogs: they aren’t going anywhere and are best eliminated.

Businesses in low growth rate industries but with dominant market share are cash cows: they aren’t growing fast but you should hold onto them and milk the profits.

Businesses with a high market share and a high growth rate are stars, the ideal business to be investing in as they should compound quickly over time.

Businesses in a high growth rate industry but made 2nd or 3rd in market share are question marks and they will either grow to become stars or fall to become dogs.

The tricky thing about most star businesses is that they tend to start when the industry is very small. It’s really, really hard to establish dominant market share in a well-developed industry but much easier in an emergent one. So typically what happens is that a star business started in a very small industry and got a first-mover advantage and was able to carry it through.

In general, people seem to over-index on the present and underestimate growth rate. An industry growing at 30% per year will be 19x larger in ten years and 374x larger in 20 years. So even starting from a very small base, compound growth really adds up.

In general, it’s important to know that competition risk is usually greater than market risk. It’s a better bet to start a business in a small, growing market that might not pan out than to try and compete in a big, established market.

Firms that sought growth by entering small, emerging markets logged twenty times the revenues of the firms pursuing growth in larger markets. The difference in revenues per firm is even more striking: The firms that followed late into the markets enabled by disruptive technology, on the left half of the matrix, generated an average cumulative total of $64.5 million per firm. The average company that led in disruptive technology generated $1.9 billion in revenues. The firms on the left side seem to have made a sour bargain. They exchanged a market risk, the risk that an emerging market for the disruptive technology might not develop after all, for a competitive risk, the risk of entering markets against entrenched competition.

Harness Emergence

A helpful idea from complexity science that is very applicable to innovation and innovative thinking is the notion of emergence.

Life on Earth started as a few single-celled organisms and over a few billion years of evolution, some pretty interesting and complex stuff emerged. Similarly, we see emergence happen in markets.

When Honda expanded into the United States, it discovered a market that it didn’t even know existed.

Honda proved just as inaccurate in estimating how large the potential North American motorcycle market was as it had been in understanding what it was. Its initial aspirations upon entry in 1959 had been to capture 10 percent of a market estimated at 550,000 units per year with annual growth of 5 percent. By 1975 the market had grown 16 percent per year to 5,000,000 annual units—units that came largely from an application that Honda could not have foreseen.”

Another example of emergence goes back to mobile phones. Once you could carry a computer in your pocket, Uber suddenly made sense. It was an emergent property of a changing technological and economic landscape.

My favorite saying for harnessing emergence: “Unexpected successes are the best source of strategy.”2

Whenever some unexpected thing happens (good or bad), there’s a decent chance that it is the result of some new emergent property that may present an opportunity.

Use your Fingerspitzengefuhl and Tinkering to Stay Attuned to Emergent opportunities

In order to innovate, you have to allocate what feels like an irresponsible amount of resources to new opportunities.

Scott Cook, Intuit’s founder, surmised that most of these [successful] small companies were run by proprietors who relied more on their intuition and direct knowledge of the business than on the information contained in accounting reports.

In other words, Cook decided that the makers of accounting software for small businesses had overshot the functionality required by that market, thus creating an opportunity for a disruptive software technology that provided adequate, not superior functionality and was simple and more convenient to use.

This is almost always the case. There is rarely good “data” for a small, but fast-growing industry. It is something people jump into based on their intuitive feeling. You want something that seems illegible to most people.

This makes sense when you appreciate the star principle and compounding. Small bets with a high growth rate can turn into very big successes. But, those opportunities only tend to exist when they are confusing and hard to understand so you have to rely on some intuitive feelings. By the time the data is clear, it’s usually too late.

Footnotes

- As noted above, Christensen may take umbrage with me using Uber as an example of Disruption because it doesn’t fit into his theoretical framework, but I find it useful and this is my blog so here we are.

- To put this in Boydian terms, double down on your fast transients.